With market volatility like we saw last week, we know everyone is wondering if this is the beginning of a prolonged sell off or even an economic recession. Here are a few key observations we see that lead us to believe this is a pause, and that the stock market is likely to reach higher market highs in the near future.

A few bullish points you may find interesting

- While the cost of credit is getting more expensive, the supply of credit is plentiful and demand is robust. Bear markets typically don’t start when the credit market is healthy.

- The yield curve is not inverted. Most bear markets start when the curve is inverted. Also, some of the biggest percentage gains have been logged just as the curve goes from flattening to inversion. We have yet to see this type of “blow off top.”

- Bull markets end in euphoria. I would argue institutional and retail investors alike are actually more pessimistic, which means this bull market is primed to grow. (1)

Q&A Addressing recent market volatility

- What is the proximate cause of the current correction? - The most proximate cause of recent market weakness has been the now obvious commitment to “normalize” interest rates. The “new normal” over the last 9 years is dead and the Trump Administration’s economic policies have killed it. To the extent to which we believe stock prices are ultimately a function of earnings and interest rates, we see the current correction as an opportunity to buy good cyclical companies at attractive prices.

- Are 2019 earnings at risk? – Though Earnings Per Share growth rates will level off next year as the anniversary effect rolls the tax cut into its fifth quarter. We continue to be focused on Earnings Before Interest & Taxes (EBIT) earnings growth rates with 2018 EBIT currently running at +11.8% over 2017, which is very healthy at this stage of business cycle.

- Tactically, are we close to putting a low? - The response from last Thursday’s rally was unconvincing – breadth was fair, but not spectacular; nor did volume skews suggest any panicked demand for stocks. All things considered, we doubt we’re through this quite yet and wouldn’t be surprised if more drama is still in front of us. Seasonality supports a postelection rally, but it’s the character of any advance (e.g., does participation broaden out, does leadership reclaim a pro-risk bias, etc.) that will be key to the strategic call. (1)

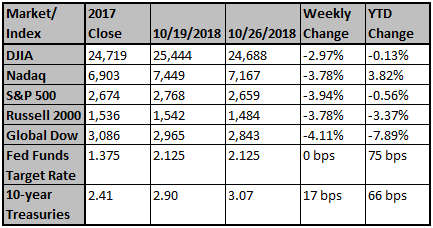

Last week "in volatile trading, the sell side sentiment pushed all of the major indices lower. Companies, though, continue to outperform analysts’ projections; of the 48% of companies in the S&P 500® Index which have already reported results, the 22.5% growth in earnings is on track as the third best performing quarter since 2010. For the week, the S&P 500® fell 3.94%; the Nasdaq and the Russell 2000® Index both lost 3.78%, and the Dow Jones Industrial Average lost 2.97%. The continued selloff in Technology stocks brought the sector’s decline (11.9%) into correction territory. Amazon and Alphabet reported earnings that were 86% and 25%, respectively, higher than earnings expectations; but revenues fell short of analysts’ estimates. Netflix, now down almost 30% from its twelve-month high, continues as the worst performer amid concerns that the company’s high debt level will impact growth as interest rates rise. Microsoft and Intel reported strong earnings and revenues yet their results were overshadowed by market sentiment; that is, the “law of large numbers” is impacting tech stocks as investors continue to expect dramatic growth despite the challenges for these megacap companies to “moving the needle.” Looking ahead, more reasonable growth valuations will require a recalibration to more realistic revenue targets.

Economic data continue to support the growth narrative; the first estimate of third quarter GDP growth, 3.5%, was slightly higher than projections; consumer spending rose 4% to the highest levels since 2014. Investors seem to believe that the combination of low unemployment, tariffs, a stronger dollar, and rising material costs may signal that the markets have reached ‘peak earnings’; higher costs will dampen revenue and earnings growth. This “broad brush” approach assumes that all market sectors move in sync; it fails to recognize that sectors are at different stages in their growth cycles. A marine transportation company reported earnings today; management made a strong case that they are only now in the early stages of recovery from the energy downturn. Barge rates and profit margins are still well below normal; utilization rates are only now recovering to the mid 90% range. An automotive company reported yesterday that the recent decline in new car sales spurs their used car business; their parts and service areas remain a major segment of their business. In addition, their truck leasing division reports increasing demand to satisfy the emerging 1-to-2 day delivery standard of e-commerce.

The selloff may reflect both the absence of progress on the geopolitical front and the disappointing Technology sector revenue reports. Tech stocks have been the ‘easy trade’ for the past several years; the sector’s market advance overshadowed corrections and bear markets in other sectors. Historically, investors often extrapolate an investment thesis until expectations become unreasonable. Now, as investors evaluate corporate earnings and commentary, they will likely begin searching for overlooked and undervalued companies. Most analysts believe that, for many companies, the selling has been overdone; active investors will likely await signs of ‘seller exhaustion’ before establishing new opportunities." (2)

Source: (1) Strategas and (2) Pacific Global Investment Management Company

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments.

Related Articles

This Time It's Different For NASDAQ

1. Popular stock momentum is driven by revenue and earnings growth rather than plain air back in the late 1990s.

How the U.S. Can Rebuild Its Capacity to Innovate

The country invests more in R&D than anyone, but it needs manufacturing, too.