The Senate just passed a new 2,700 page $1 trillion bipartisan infrastructure bill. From the Senate, the bill moves to the House where Speaker Pelosi has suggested she will not take up the bill until Senate Democrats pass a separate (and much more expensive) package without GOP votes under a budget reconciliation process. Because this bill includes the largest tax increases since 1968 (nearly three times the size of the tax increases enacted by Reagan, Bush, Clinton, and Obama), we feel it is important to share some of the facts that we now know about the bill. We also feel it is important to share that this is also really the first time we are raising taxes on capital in 50 years and the first time Congress will raise corporate taxes and capital gains taxes in the same legislation since the early 1950s. Because the information discussed is “policy,” it is very difficult to bring this information to you without politics entering the discussion, but we think our Research Partners at Strategas have done the best job they could at keeping this discussion as apolitical as they could.

We also want to highlight that increased corporate taxes will reduce corporate earnings. Because stocks trade at some multiple of their “earnings,” as earnings fall, it is only natural to expect the stock market’s growth to slow down too. Additionally, most analytical models find that higher capital gains tax often leads to less investment over time because the net return of the investment is diluted. When we increase both corporate taxes and capital gains at the same time, we expect a reduction in “real” long-term equity returns to some degree. Said plainly, an increase in taxes will almost surely create a drag on investment portfolios.

PROGRESSIVES GET THEIR TURN TO INCREASE SPENDING & RAISE TAXES

With a divided 50/50 Congress, the nature of power in Washington swings back and forth over fiscal policy. For the past three months, Washington has been consumed with a bipartisan infrastructure package and often to the dissatisfaction of the progressive wing of the Democratic Party. This focus on bipartisanship will shift this morning with the Senate passing the bipartisan package around 11am and then moving immediately towards passing the FY 2022 budget. Passage of the FY 2022 budget opens the budget reconciliation process, thereby allowing Democrats to pass fiscal legislation on a partisan basis with no Republican votes. The budget instruction allows for $1.7 trillion of net spending. Coupled with the bipartisan infrastructure package, this gets us close to our base case of $2.5 trillion in spending and $1.7 trillion in tax increases.

Senate Budget Proposal Creates The Window For A Major Expansion of Government Spending & The First Major Tax Increases On Capital In 50 Years:

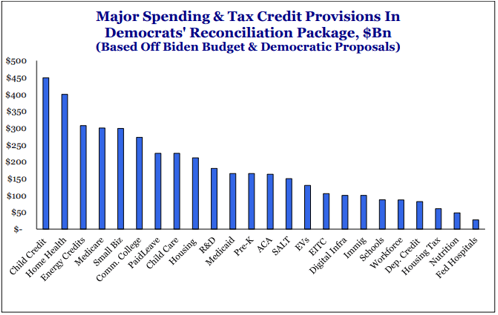

Yesterday’s budget release was a sign that progressives will get their turn to go big by passing a $3.5 trillion spending package. New spending will include a heavy focus on climate change, health care, and income transfers. The budget also calls for $1.7 trillion of offsetting tax increases and/or spending cuts. This includes tax increases on income, capital gains, dividends, estates, and corporations. Other ideas include taxes on companies that contributed the most to climate change in previous years, a methane tax, and deferred income limits for asset managers.

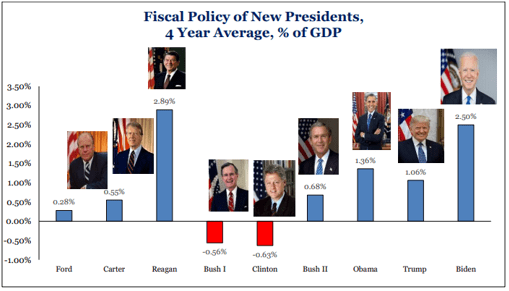

Budget Proposal Creates The Fiscal Space For The Largest Expansion of Fiscal Policy Since Reagan, Even Factoring In Tax Increases:

Combining March’s COVID package, the bipartisan infrastructure deal, and this budget, Biden is proposing a net fiscal spend of 2.5% of GDP annually. This would mark the largest expansion of fiscal policy since Reagan’s first term 40 years ago. The nature of the Reagan fiscal policy expansion was lower tax rates and falling inflation. Conversely, Biden is moving towards more government spending with rising inflation. The model is different, but the size of this level of spending rivals the mid-1960s.

Tax Increases Are Quite Different Than Tax Increases Over The Past 40 Years:

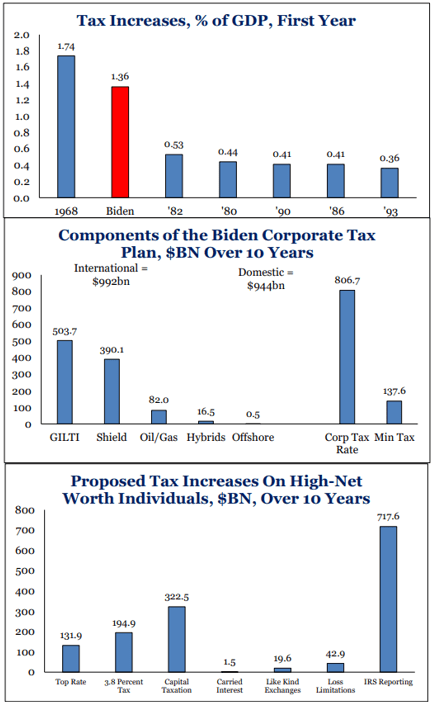

Even under a compromise scenario, tax increases will be the largest since 1968 and nearly three times the size of the tax increases enacted by Reagan, Bush, Clinton, and Obama. This is also really the first time we are raising taxes on capital in 50 years and the first time Congress will raise corporate taxes and capital gains taxes in the same legislation since the early 1950s. Some investors believe the tax increases are manageable, and they could be with an accommodative Fed and the tax increases phased in overtime, but what we are doing is outside the normal range of nearly every professional investor’s lifetime. Fiscal policy from 1966-1976 was largely viewed as counterproductive to economic growth. We are replicating those policies.

The Bipartisan Infrastructure Package Has Given Cover To Moderate Democrats To Vote For A Progressive Budget:

We get the sense that Senators Sinema and Manchin are willing to move the process forward by voting for this progressive budget authorization now that Republicans have given the moderates cover by passing a bipartisan infrastructure package. The key metric to watch in the early part of the budget debate this week is Republican amendments to cut down the size of the spending and/or tax increases. Manchin and Sinema have said they do not support $3.5 trillion of spending. Republicans can call them out by offering an amendment and forcing them to take a position. Our sense is that moderate Democrats will argue over the “net” and say they are voting for a $1.7 trillion budget.

Progressives Have The Power For The Budget, But This Power Will Shift Back To The Moderates During The Legislative Process:

This shift to the progressives will likely be temporary for the budget negotiations. But as we move back to the actual tax and spending legislation in 4Q, the moderates will gain the upper hand, and will likely seek to water down the spending and tax increases. Still, we expect Democrats to get a large share of what they are trying to accomplish, particularly on health care spending, renewable energy spending and tax credits, and new income transfers such as a multi-year extension of the child tax credit.

Timing of the Debate Will Impact The Effective Date For Tax Increases:

Democrats hope to have their budget passed by the end of September. Looking at the timing of previous reconciliation measures, legislation usually takes six to eight weeks to pass into law after the budget passes. This puts the timing of the legislation around late November/early December. The later in the year, the harder it is to make the tax changes on corporate and individual income retroactive. The budget does give some space so the budget does not need money immediately. Capital gains could still be retroactive and the September 15th deadline for the committees to report policy is now the most likely effective date for a capital gains tax increase.

OUR BASE CASE ON TAXES

Individual Income:

- Top marginal income tax rate increases from 37 to 39.6 percent and this top income tax rate will be placed on a greater portion of a taxpayer’s income.

- Some tax increase on business income that is currently taxed at the individual income level. This could be the removal of the 20 percent tax deduction for small businesses or a new 3.8 percent tax placed on top of the top marginal tax rate.

- Increase in the State and Local Tax Deduction (SALT), which is important to Speaker Pelosi (CA) and Senate Majority Leader Schumer (NY) as well as the moderate Democrats in higher income districts who are worried about voting to raise income, cap gains, and estate taxes on their constituents.

- More IRS funding and IRS authority of financial transactions. This could be quite a large revenue raiser depending on how it is structured. · These changes are likely to be effective for CY 2022 based on our expected timing of the legislation passing into law.

Capital Gains/Dividend Income/Real Estate

- Raise the capital gains and dividend tax rate to approximately 28 percent from the current 20 percent today.

- We believe the effective date for this will be around the time of enactment or when the legislation is introduced. September 15th is the date that the Senate Finance Committee is required to report its proposal and is now an option for the effective date. There is still a possibility that the rate could be retroactive further back, but the delay in passing the legislation is delaying when the effective date could be.

- Removal of carried interest has been proposed. More than 80 percent of carried interest is generated from real estate, and our sense is that Congress is more focused on a larger tax revenue raiser: ending deferred income of asset managers. · Biden has proposed to get rid of 1031 like-kind exchanges. We have a tough time seeing that getting the votes, but it will be on the table.

- We expect to see new limits on IRAs due to the recent news articles of Peter Thiel having $5bn in his Roth IRA.

Estate Taxes

- We expect the estate tax rate to be lifted and the exemption to be lowered. Note that this is very different than what Biden proposed. Biden has proposed moving from a step up in basis to a carryover basis and imposing a new unrealized capital gains tax at death for gains over $1mm. Both ideas are not getting the traction needed to pass in a narrowly divided Congress. We heard some talk that Congress may insert the Biden proposals, but have them kick in five years from now. This is a way of using the revenue for spending, but not having to deal with the changes immediately. As such, we are not discounting the Biden proposal, but it is less likely to be something that impacts in the short term if anything.

Corporate Taxes

- Increase in the corporate tax rate from 21 to 25 percent (effective CY 2022).

- Increase in taxes on US multinationals to 18 percent with fewer deductions (effective date will depend on global OECD tax negotiations).

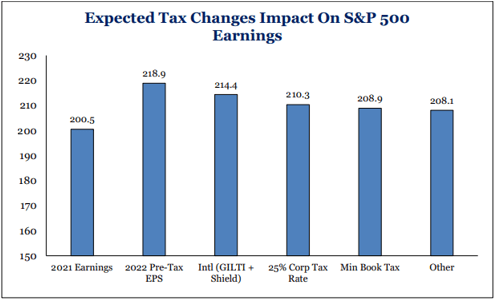

- We are anticipating the combined corporate tax increases will cut the growth rate of S&P 500 earnings in 2022 from 9.2 percent to 3.7 percent.

- We also expect Democrats to attempt to enshrine the global minimum tax deal as part of the reconciliation package. This would include a 15 percent global tax rate. The other changes being negotiated at the OECD are treaty based and would likely require bipartisan approval.

Energy Taxes

- Proposals to remove the intangible drilling credit are unlikely to pass, but smaller tax deductions are likely to be removed from the industry. · There will be significant attention around the proposal to tax companies that were responsible for 0.5% of global carbon and methane emissions since 2000. This could be a $6bn tax on XOM, CVX, and fossil fuel companies. New proposals like this usually don’t pass the first time around.

- The methane tax is more developed, but probably also unlikely to go through. Still, this proposal to tax $1,800 per US ton of fugitive methane emissions from oil and gas producers and midstream could gain more support. The proposal, based on 2015 emissions, will likely raise hundreds of billions of dollars. We would not be surprised if a compromise emerged allowing a phase-in of the tax and allowing for a later year benchmark of methane emissions, which will be lower.

- You pull all of this together and you get roughly $1.5 to $1.8 trillion of tax revenue over 10 years. Our belief is that the first $600bn is a done deal, the second $600bn becomes tougher, and the third $600bn will be excruciatingly difficult. Congress will likely need to play with the budget window and employ dynamic scoring because the demand for spending is so much greater than the taxes available. Democrats will also look for pharma savings to enhance the tax revenue.

External Catalysts To Keep An Eye On

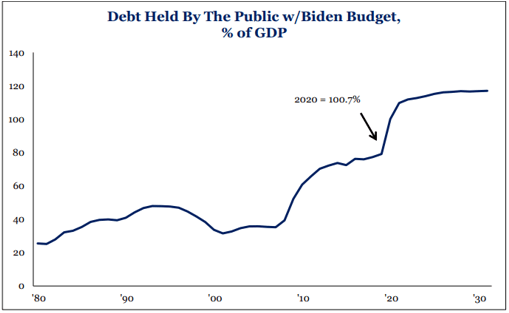

- Debt Ceiling: Democrats have complete control of the government and should be able to raise the debt ceiling through the budget reconciliation process. But the Democrats probably do not have the votes to increase spending by $3.5 trillion and raise the debt ceiling. We are headed for a game of chicken as Republican Senate Leader McConnell refuses to help Democrats with the debt ceiling if they are going to pass $3.5 trillion of new spending on a partisan basis. Republican insistence on not helping may force the entire package to be scaled down if Democrats need to go it alone on the debt ceiling.

- OECD Tax Negotiations: The Biden Administration is pushing for a global minimum tax deal in order to get other countries to impose taxes on their multinationals. The reason for this is that members of Congress are worried that if Congress raises taxes on US multinationals, US companies will be at a competitive disadvantage. As such, Treasury Secretary Yellen is trying to get all countries to raise their taxes at the same time. The goal is to have this deal in place by October, ahead of the US tax legislation passing. If this timeline slips, or even if countries hedge on when they will pass their tax increases, this could impact a significant portion of the US corporate tax increases.

- California Recall & VA Gubernatorial Elections: Next month voters in California will vote on the recall of Governor Newsom. If Newsom loses, that could be a real sign that the political environment is shifting and could impact moderate votes. The Virginia governor’s race in November could be a bigger sign should the Republican win. Off-year elections have been a good sign of whether presidents will lose their first midterm elections. Many moderate Democrats may be unwilling to raise taxes at this scale if they believe they are vulnerable in next year’s midterm elections.

- Inflation & COVID: President Biden believed he needed to get COVID under control and get the economy back on track. For the first six months, he was on that pace. But COVID has heated up, which may pressure Congress for more short-term stimulus. At the same time, inflation is now a bigger concern for voters than unemployment and this could lead to a smaller package if this trend continues.

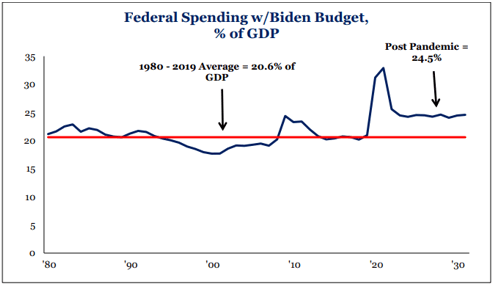

BIDEN IS PROPOSING THE LARGEST FISCAL EXPANSION SINCE REAGAN 40 YEARS AGO

NEW PROPOSED SPENDING IS FOCUSED ON BOLSTERING THE SOCIAL SAFETY NET

TO PAY FOR THE NEW SPENDING, BIDEN IS PROPOSING THE LARGEST TAX INCREASE SINCE 1968

HIGHER CORPORATE TAXES WOULD SHAVE MORE THAN $10 OFF 2022 S&P 500 EARNINGS GROWTH

Have the 2017 tax cuts worked?

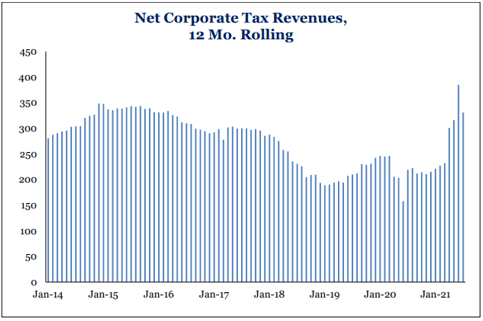

Lowering Corporate taxes increased tax revenue

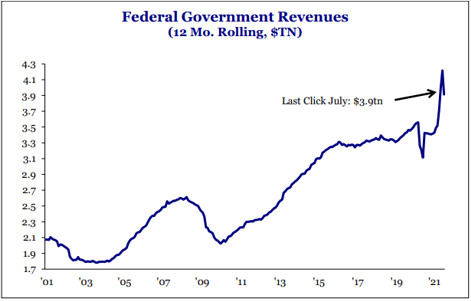

TAX REVENUE IS UP 14% Y/Y

CORPORATE TAX REVENUES NEAR AN ALL-TIME HIGH WITH A 21% CORPORATE TAX RATE

DESPITE STRONG JOB GROWTH, CONSUMER STOCKS STRUGGLING AS STIMULUS ROLLS OFF, INFLATION RISES

Friday’s employment report was terrific. We continue to believe that overly generous unemployment benefits, schools, and vaccine hesitancy are the factors holding back employment from its full potential. There were not many developments on the latter two items in July, but half of the states ended their overly generous UI benefits. This should have the effect of helping to boost employment. It’s been telling, however, that the consumer stocks levered up to more stimulus have moved meaningfully higher with strong jobs, wages, and the child tax credit being implemented. This is likely because the loss of stimulus aid will be greater than the income gained by moving into employment. Personal savings are needed to carry the consumer.

Source: Strategas

Sincerely,

Fortem Financial

(760) 206-8500

team@fortemfin.com