The S&P suffered its first quarterly decline since the depths of the pandemic in Q1 of 2020 (-5.0%). Growth (-8.6%) meaningfully lagged value (-0.6%). The biggest development in Q1 was the dramatic repricing of the Fed rate hike path and expectations for an earlier start to and more aggressive balance sheet runoff phase. Late in the quarter, markets priced in a ~80% probability of a 50bp rate hike in May and ~200 bp in cumulative hikes by the end of 2022 following the 25 bp liftoff at the March meeting. This shift was driven by concerns about elevated and persistent inflation pressures. A 40-year high in the CPI highlighted such concerns. The hawkish Fed policy shift drove a big backup in bond yields, and Treasuries suffered one of their worst quarters on record. Curve inversion drove worries about potential recession and a Fed policy mistake. Q4 earnings season marked a fourth straight quarter of 20+% earnings growth. Geopolitical tensions became a much bigger issue for the market as the quarter witnessed Russia’s invasion of Ukraine. Energy stocks surged nearly 40%, its biggest rally on record. Treasuries sold off sharply, with 2-year yields up over 150 bp to 2.30% and 10-year yields up over 80 bp to 2.33%. WTI crude rallied more than 30%.

Intellectuals and politicians often try to verbally summarize or justify conventional thinking in pithy ways. Milton Friedman (in 1965) and Richard Nixon (in 1971) both said different versions of the phrase "we are all Keynesians now."

John Maynard Keynes, one of the most famous economists of all time, supported deficit spending and government manipulation of economic activity. Friedman and Nixon were describing the thoughts behind the implementation of Great Society redistribution programs and an inflationary monetary policy designed to offset the cost of those programs.

If economic policy was Keynesian in the 1960s and 1970s, as policymakers stopped believing in free markets, we are certainly all Keynesians now. COVID spending and monetary policy are a clear continuation of this economic thinking.

It all began in 2008, when the Bush and Obama Administration combined spent $1.5 trillion of taxpayer money to "rescue" the economy and the Federal Reserve started Quantitative Easing. That blueprint of policy response to the Panic of 2008 was used to respond to COVID shutdowns. This time the Federal Government borrowed at least $5 trillion to spend and the Fed increased its balance sheet by over $4.5 trillion.

As a result of the Keynesian policies of the 1970s, the U.S. experienced stagflation (slow growth and high inflation) – with both unemployment and inflation peaking in the double digits. Right now, inflation is 7.9% and the unemployment rate is 3.6%. So while inflation is clearly here, signs of stagflation are harder to find.

That doesn't mean economic growth isn't being impacted. There are multiple forces to analyze and untangle to understand everything that lockdowns and government largesse have done.

First, the US economy was artificially boosted by borrowing money and distributing it through PPP loans and pandemic benefits. Case in point, retail sales are up 25.2% between February 2020 and February 2022, while industrial production is up just 2.3%, and the US has 1.6 million fewer jobs than it did pre-lockdown. The good news is that unlike the Great Society programs, the spending done in response to the Financial Crisis and COVID-19 are not all permanent increases in entitlements. Some of our COVID response spending is likely to be permanent, but not all of it.

Second, the M2 money supply has increased more than 40% since February 2020, as the Fed renewed QE and monetized deficit spending. In other words, a great deal of that spending was paid for out of thin air.

The impact of these policies was like giving morphine to an accident victim. The economy was dramatically damaged by the lockdowns, but the morphine masked the pain. All that pain-killer stimulus boosted sales and profits. This year, without new spending legislation and as the Fed starts to reverse course, the economy will lose its morphine drip.

On the surface, this suggests that the economy could be in trouble...and with the 2-year Treasury yield now above the 10-year Treasury yield (an inverted yield curve), many think the US faces a recession this year.

But this ignores the impact of the third factor in play – the reopening of the economy. It is clear, at least to us, that very generous pandemic unemployment benefits had a massive impact on employment. In fact, the "Great Resignation" (people just dropping out of the workforce) had a lot to do with these benefits. While it was never the case, many thought the Build Back Better spending bill would keep the checks coming. Now that BBB appears dead, those people are heading back to work. In the first three months of 2022, 1.69 million jobs have been filled. This year will likely total 4 million jobs, or more.

So, even though the Fed will be lifting rates and Keynesian deficits will be smaller, the economy will expand in 2022 and profits should continue to rise. Unfortunately, our forecast is that real GDP growth will remain under 3%, while inflation remains over 5%. This is reminiscent of the 1970s, and once the reopening from lockdowns is over, the full impact of these policies will be felt.

The inversion in the yield curve suggests the bond market thinks that if the Fed lifts short-term rates to 3% or so, it will be forced to cut rates again. This may be true, but we think inflation will prove a more persistent problem than the Fed or the bond market have priced in.

The US is now stuck in a Keynesian dilemma of its own making. The way out is to cut spending, cut tax rates, cut regulation, and tighten money enough to stop inflation. Because in the end, Keynesian policies don't create wealth...free and open markets do.

Source: Brian Wesbury First Trust

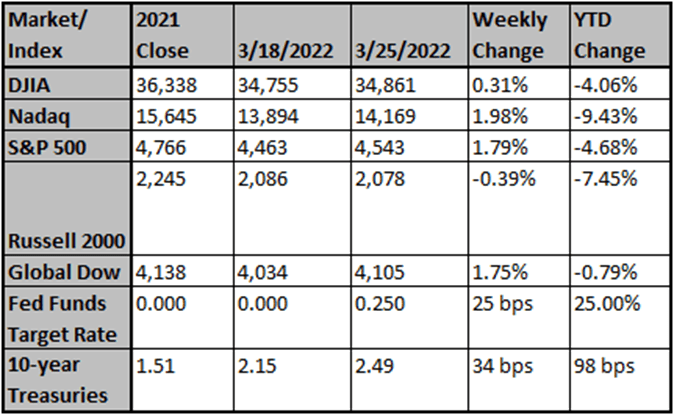

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments. Data provided by Refinitiv.

Sincerely,

Fortem Financial

(760) 206-8500

team@fortemfin.com

Latest News

Markets Expect 25-Basis-Point Fed Rate Hike in March 2022

The markets expect the FOMC to vote for a 25-basis-point fed funds rate hike at its meeting on March 15-16, 2022.

Investopedia

Eyes on Inflation, Shoppers Cut Back on Staples

American consumers are starting to cut costs on mainstays from toothpaste to baby formula as inflation hits a swath of the economy that had thus far proven resistant to substantial price ...

The Wall Street Journal

Gas prices trend lower following petroleum reserve release

The price of a gallon of gasoline continues to move lower after hitting a high two weeks ago.

Fox Business