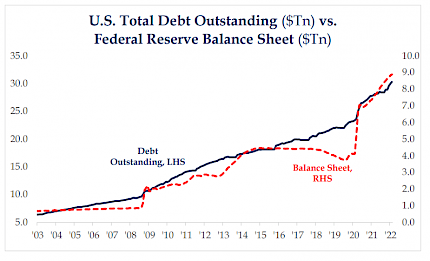

For econometricians and other expensive experts, it remained a mystery why a quintupling of the assets on the Fed's balance sheet between 2008 and 2014 led to ever greater securities prices and no appreciable increase in the prices of goods and services. In a classic case of a remedy being the hair of the dog that bit you, the solution for many central bankers was to double down on policies that did not work as intended. Other central banks, like the Bank of Japan, went a step further by adopting negative policy rates. The results were disastrous. In yet another example of how economics is not hard science, like let’s say chemistry, Japanese savers did not take more risk in response to negative deposit rates – they took less. In fact, the only appreciable inflation was seen in the sales of safes. Contrary to what the financial engineers expected, the first move of the salaryman was not to execute an exotic carry trade but to make a trip to the bank and withdraw cash to put into their new home safe. Ironically, lower rates led to lower inflation as the banking system shrank.

Today, one wonders whether we might not be on the flip side of this phenomenon. Given the fact that negative real yields have funded a number of dubious businesses that provide goods and services at cost or less, the investor now must consider whether it is possible that higher and more variable interest rates could actually lead to higher inflation. How could this occur?

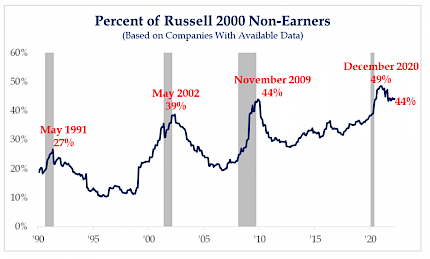

One of the unintended consequences of the quantitative easing era has been a surfeit of companies who consistently fail to produce profits in good times and bad. In a world of excess savings, investors seeking higher yields provide a direct subsidy to consumers who will gladly accept taxi rides and food delivery services below the rate at which they would be sustainably profitable. This has, of course, been a difficult time for the active manager (particularly hedge funds) and the legacy business without such a privilege alike. Sears wound up being a poster child for this phenomenon as the financial markets needed to plunge a crucifix through the heart of the company to allow it to pass from this mortal coil. In any normal business cycle before the advent of quantitative easing, higher interest rates and an increasing cost of capital for marginal companies would lead to either failure or consolidation, freeing up capital for more productive companies and technologies.

If we are indeed on the precipice of a regime change in which we are witnessing the end, at least for a while, of quantitative easing, one would suspect that more traditional companies with solid balance sheets will be able to consolidate market share as the tide of easy money goes out. This consolidation will likely lead to greater pricing power for companies that survive in certain industries like retail and transportation. Thus the great irony of higher rates could indeed be higher inflation for consumers who can no longer depend upon an indirect subsidy from the global capital markets.

There is also little doubt that the inexorable move toward globalization that started with the fall of the Berlin Wall is coming to a rather abrupt end. We can think of no greater transformation in terms of international standing and reputation than China's role as an economic partner and perhaps rival to that of a potential enemy in the aftermath of the pandemic. The gap between elite and popular opinion has narrowed considerably on this issue in the past six years. Russia's attack on the sovereign state of Ukraine has only served to put a finer point on the lie that was the idea that greater trade and communication had the ability to transform countries bereft of Western values like democracy and self-determination into "citizens of the world" acting in good faith. It was, of course, worth a shot, but it seems unlikely that the "post-World War II international order" will be restored any time soon. To the extent to which globalization was a significant driver of lower inflation over the past 25 years, this is not an insignificant development for the U.S., the world's greatest net importer of goods. If there is good news in this for the country, in my view, it is the potential to restore the standing of the American middle class who do not possess a college education. Of course, the cost of doing business in the U.S. will make it unlikely that it could ever compete with developing markets in low-end manufacturing. Still, there is a chance that, with the proper incentives and political leadership, and foresight, America can develop certain high value-added industries that restore the country's understanding of and respect for the dignity of skilled labor. (Given the world as it is rather than the way we may wish it to be, oil and gas exploration and production should be a natural beneficiary of such a trend.) This, in turn, may indeed strengthen the social fabric of a country that has appeared, in recent years, to be fraying. In the end, this may lead to lower profit margins and the emergence of quality factors as the basis upon which investments are made. There will, no doubt, be some coastal elites who may mourn this transformation. But for the rest of us, it may not be all bad. Some things have a value that cannot be measured in dollars and cents.

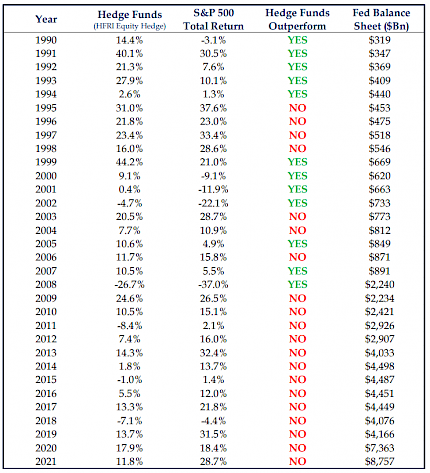

Q.E. ERA HAS MADE ACTIVE MANAGEMENT DIFFICULT

Source: Strategas

Sincerely,

Fortem Financial

(760) 206-8500

team@fortemfin.com