Late last week, President Biden announced he was going to release 55 million barrels of oil from our strategic oil reserve to combat high energy prices and inflation. Because we currently use 18mm Barrels of oil per day in the U.S. we are confident there will have to be further actions to solve the high price of oil (and its contributions to the inflation we have been seeing over the last few months). Although the announced policy attempts to bring down energy prices, we don't believe it will be successful long-term. The immediate response from OPEC was a counter-response suggesting they may act to push the prices up. Despite the back and forth with OPEC over oil prices, they plunged at the end of the week on renewed global health concerns due to the Omicron variant and renewed travel restrictions.

As the World Health Organization (WHO) named variants of the coronavirus, “officials turned to the Greek alphabet … When it came time to name the potentially dangerous new variant that has emerged in southern Africa, the next letter in alphabetical order was Nu, which officials thought would be too easily confused with ‘new.’ The letter after that was even more complicated: Xi, a name that in its transliteration, though not its pronunciation, happens to belong to the leader of China, Xi Jinping. So they skipped both and named the new variant Omicron.” (NYT)

We do not know how significant the new virus variant will be medically. “Dr Angelique Coetzee, chair of the South African Medical Association … said it was ‘premature’ to make predictions of a health crisis. ‘It’s all speculation at this stage. It may be it’s highly transmissible, but so far the cases we are seeing are extremely mild,’ she said.” (Guardian)

But restrictions with economic effects are already taking place.

Numerous countries have applied travel restrictions, (eg, U.S., U.K., E.U., Switzerland) with some stopping the passage of foreign travelers outright temporarily (Israel). Mandatory quarantines make business travel difficult (if not impossible) in the near-term. The goal appears to be to buy several weeks of time, for scientists to assess the situation.

Moderna’s Chief Medical Officer Paul Burton said a new shot could be available early in 2022. “‘We should know about the ability of the current vaccine to provide protection in the next couple of weeks,’ Burton said Sunday on the BBC’s ‘Andrew Marr Show.’ ‘If we have to make a brand new vaccine, I think that’s going to be early 2022 before that’s really going to be available in large quantities.’” (Bloomberg)

Central banks had been under increasing pressure to deal with inflation. The decline in global energy prices helps that particular issue near-term, but not in a good way. Part of the problem has been the shift in spending to goods vs. services (clogging up ports & supply chains). Services spending resuming could have removed some of this pressure. That looks partly delayed now.

It’s not just travel services. Healthcare services have already been strained. NY Governor Hochul “announced a State of Emergency Friday night to prepare for, and attempt to avoid, a surge in the Omicron COVID variant. … Along with that executive order, the Department of Health is allowed to limit non-essential surgeries and procedures for hospitals at limited capacity … The new protocols will begin Friday, December 3rd and will be reassessed in January.” (WWNY)

The U.S. economic data had fortunately shown some momentum (pre-variant). U.S. real GDP was revised slightly higher to a 2.1% q/q annual rate in 3Q. But the real news is about what’s happening in 4Q. Weekly jobless claims might have been affected by some seasonal adjustment issues, but the drop to 199,000 last week (!) was indicative of a broader package of improving data. Core cap goods orders rose +0.6% m/m in Oct. Real (inflation-adjusted) consumer spending was up +0.7% m/m in Oct., and while some of this may have been sales pulled forward from later holiday shopping, there’s a clear indication that demand was solid. New & existing home sales rose m/m in Oct. Tracking estimates for 4Q real GDP in the U.S. are at +8.6% q/q A.R. (!)

This is true even though consumer sentiment remained weak at 67.4 in the Nov U of Mich survey. We continue to watch what consumers do vs. how they say they feel.

Bottom line: markets which had priced in 3 or more Fed rate hikes in 2022 look to have overshot the mark, based on recent developments. Yet inflation concerns still matter to consumers, both economically & politically. Continued disruptions in goods/services and labor markets mean the inflation story is not finished yet.

True, as we’ve mentioned previously, high prices are not perpetually rising prices, and y/y comps should help put a top in the inflation rate (inverse base effects) in 2022. Falling energy prices will play a role in this now.

Then, central bankers will have to decide what to do with this increasingly-complicated profile. Rate hikes should still occur in 2H of 2022, as inflation is becoming stickier, and this tightening still sets the U.S. economy up for a 2023 “mid-cycle slowdown” in our view.

It is still the base case that supply can rise to meet demand. But central bankers are facing an increasingly difficult task of getting from above-trend growth (inflationary) to below-trend growth (disinflationary) without going too far. The path got bumpier this past week.

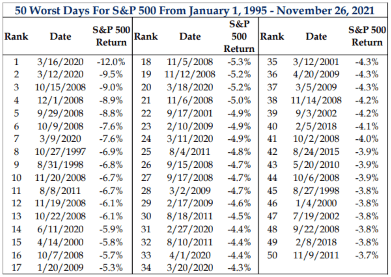

Friday’s Sell-Off Of -2.3% Not Even Close To Being In The 50 Worst

With the S&P 500 down -2.3% on the shortened trading day Friday, it was the worst one-day loss for the index since February. Historically speaking, this decline was not even close to cracking the top 50 worst days for the S&P since 1995. However, ranking 208 out of 6,775 trading days is still painful.

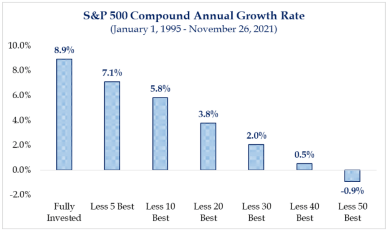

A Reminder That Market Timing Is Incredibly Difficult

Although it’s easier said than done, ignoring the day-to-day gyrations in the market and headlines for rationalizations of sell-offs is often the best strategy. We would all love to time the market to miss the worst days and be invested only on the best days, but it is impossible. As the chart below shows, missing just the five best days over the last 25 years would result in annualized returns 1.8% less than being fully invested.

Average Stock Is Down -13%, In-Line With Historical Median

After last Friday’s decline, the average stock for the S&P 500 is down -13%, in line with the historical median. If this were to turn into a deeper correction, there could be significantly more pain to be had before the market reaches the -2 standard deviation mark, which historically has been a decent barometer of entry points during a major sell-off.

Source: Strategas

Chart reflects price changes, not total return. Because it does not include dividends or splits, it should not be used to benchmark performance of specific investments. Data provided by FactSet.

Sincerely,

Fortem Financial

(760) 206-8500

team@fortemfin.com

Latest News

Omicron's Market Risk Is Already Looking Overdone

Calm is returning, unless you count holiday travel stress. But the new variant's bigger impact could be on monetary policy, with the Fed unable to

Bloomberg

Food, gas prices pinch families as inflation surges globally

Rising prices are fueled by high energy costs and supply chain disruptions.

ABC News

The Tell: Oil could hit $150 a barrel with OPEC+ 'in the ...

Oil futures can shake off the omicron-inspired selloff and "overshoot" to the upside, potentially "overshooting" to $150 a barrel in 2023 with OPEC+ "firmly in the driver's seat," say ana...

MarketWatch