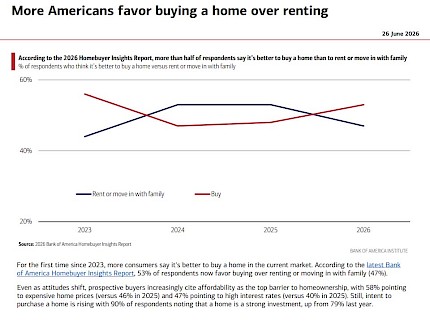

However, it is a bit challenging due to increased regulations and interest rates. This year’s Homebuyer Insights Report survey data reveals meaningful changes in attitudes toward homeownership. The study finds that for the first time since 2023, more Americans favor buying a home (53%) over renting or moving in with family (47%). Even as attitudes shift, prospective buyers increasingly point to affordability as the top barrier to homeownership, with expensive home prices (58%, … View More

June 2026

Post 1 to 6 of 6

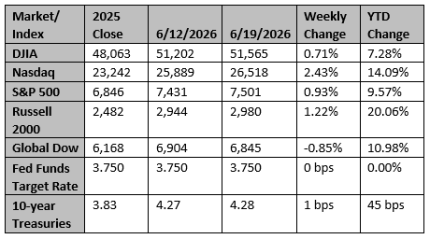

A deal to extend the ceasefire in the Middle East has finally been agreed, allowing energy prices to decline further and risk-asset markets to resume their pre-war bull run. The history of the Middle East points to inevitable bumps ahead. A lasting peace has not been achieved, and some of the players are not agreeing to stop at this juncture. Should investors expect setbacks ahead? Summary Equities were higher last week with the DJIA and Russell 2000 hitting record highs, while the S&P… View More

With what appears to be a deal with Iran taking shape and the reopening of the Strait looking increasingly likely, the two most important questions we are asking ourselves are: 1) How will global inflation expectations respond, and 2) will markets revert to the trends and themes that were working before the conflict began? Easing Inflation Expectations to Provide Rate Relief The direction of global inflation expectations will be one of the most important variables to monitor in the coming … View More

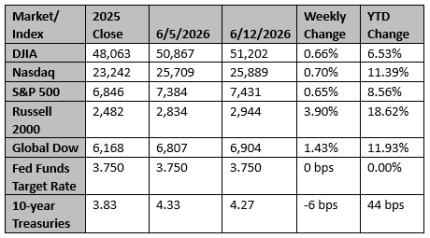

The job market was surprisingly strong in May, with non-farm payrolls growing 172,000, beating even the strongest forecasts for the month. As a result, the futures market is now pricing in a quarter-point rate hike later this year and, more likely than not, another quarter-point rate hike sometime in 2027. But we think a rate hike would be ill-advised and unlikely. First, this is a good employment report, but not a “barnburner.” Barnburner job growth is 300,000 to 400,000 per month. Even Ke… View More

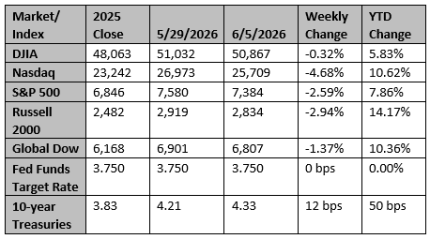

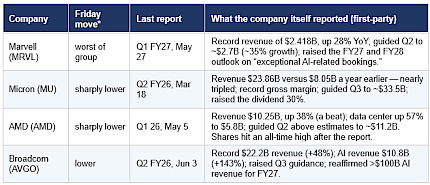

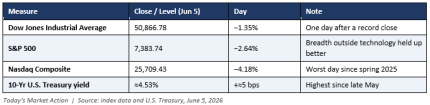

Loud Headlines, Intact Fundamentals It was a loud few days. On Friday, the Nasdaq Composite fell 4.18% — its worst single day since April 2025 — as a violent selloff in semiconductor and AI-related shares dragged the major indexes lower, with the Philadelphia Semiconductor Index down 10.26%, its steepest drop since March 2020. Over the weekend, the conflict in the Middle East escalated again, and South Korea’s market, heavily concentrated in memory chips, opened sharply lower to start… View More

A Strong Jobs Report, an AI-Led Selloff, and What the Evidence Actually Says In our June monthly commentary we flagged June 5 as the date to watch for the wage-and-jobs leg of the cycle. It arrived today, and the market’s response pulled two of our running threads into a single, unusually sharp session. The May employment report came in far stronger than expected, Treasury yields jumped, and equities sold off hard — led almost entirely by the artificial-intelligence and semiconductor na… View More