Strong 3Q Reporting Season So Far, 2026 Overall Expectations Little Changed With 29% of companies reporting this earnings season, overall results have been strong. About 87% of companies have beaten earnings estimates, and 82% have exceeded revenue expectations. Financials have shown the most significant improvement in earnings growth forecasts, rising to 21% from 12% at the start of the quarter. Materials have also strengthened, with growth estimates increasing to 19% from 14%. For the overall… View More

Authors

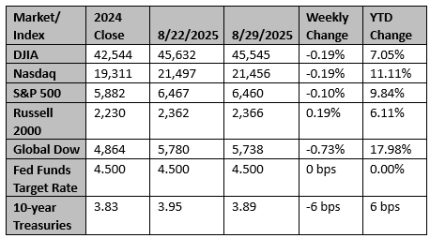

Fortem Financial

Post 41 to 50 of 630

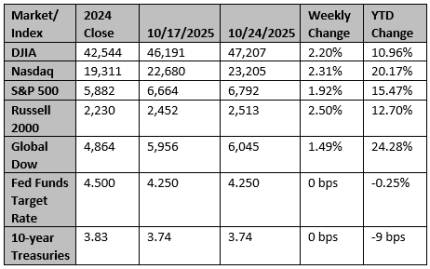

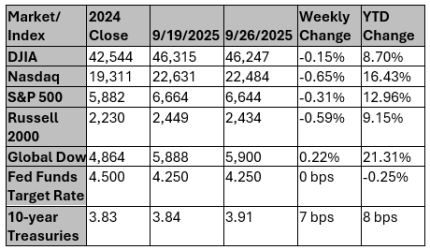

Summary Stocks rebounded in a volatile week (S&P 500 +1.71%) following the rout two Fridays ago. 3Q25 earnings started strong, led by big banks. Volatility resulted largely from U.S.-China trade rhetoric. Best sectors were communication services (+3.64%) and real estate (+3.46%); biggest laggard was financials (+0.03%). The High-Risk Bull Market Continues The October Fed Beige Book points to slowing growth as uncertainty continues to weigh on activity. The September ISM Services In… View More

Over the past two and a half decades, the federal government has buried taxpayers under a mountain of debt, now approaching $38 trillion. During this time, the key problem has been spending, not a lack of tax revenue. Over the past 25 years, taxes have remained relatively stable as a share of GDP, while spending has continued to rise. It's estimated that spending was 23.2% of GDP in the year ending September 30 (Fiscal Year 2025) versus 17.7% in 2000. In other words, the reason there is a debt … View More

Key Takeaways In the absence of the usual monthly payroll report, the September ADP report contracted by 32k jobs, missing expectations and extending the trend of weakening employment. The September Dallas Fed Manufacturing Survey missed expectations, confirming weak growth and employment momentum. Consumer confidence fell again (from 97.8 to 94.2), reconfirming weakening labor signals. It is hard to justify the resumption of a Fed rate-cutting cycle when the economic expansion is dura… View More

Congressional Democrats have limited influence over President Trump’s policy agenda, but government funding requires 60 votes in the Senate, giving them leverage since Republicans hold just 53 seats. Votes will be used as leverage, putting the US government into a shutdown at midnight tonight. Democrats' Position: ACA Subsidies Democrats are pushing to extend enhanced Affordable Care Act (ACA) tax credits, which expire at the end of 2025. They view this as an important policy priority an… View More

Earnings Projections Revised Upward for Q3, Contrary to Historical Trends As we near the end of the third quarter this week, optimism regarding Q3 earnings growth remains strong. Estimates have been revised upward throughout the quarter, now projecting an 8.8% increase, which goes against the historical trend of downward revisions. Seven of the eleven sectors are anticipated to report positive earnings growth, with four sectors expected to see growth in the mid-to-high teens. The technology se… View More

The loss of momentum in U.S. payroll job growth has been a concern. The FOMC statement noted last week that "job gains have slowed, and the unemployment rate has edged up but remains low" and followed that up with "the Committee … judges that downside risks to employment have risen." However, initial claims falling to 231,000 (240,000 on the 4-week average) were reassuring last week. Factoring out recent noisy readings due to fraud in TX, claims indicate economy-wide firing remains limited. U… View More

What is M2: M2 is a measure of the money supply that includes M1 (currency, demand deposits, and other liquid deposits like checking accounts) plus savings deposits, money market accounts, and certificates of deposit (CDs) with maturities of less than $100,000. It represents a broader measure of money available in an economy for spending and investment. If a tree fell in the woods, but the data said it didn’t, does it really mean anything? Despite what appeared to be relatively solid data, m… View More

Recent economic indicators suggest growing concerns about a potential recession. With calls for such an event expected to intensify. A weak jobs report has solidified expectations for an interest rate cut, as policymakers aim to stimulate economic activity. Analysts anticipate that discussions surrounding a recession will amplify in the near term, driven by persistent labor market challenges and broader economic uncertainties. Key Points: Recession Concerns: Emerging signals indicate a … View More

U.S. real GDP was revised higher in 2Q, which helped keep NIPA corporate profits in positive territory (+1.7% q/q and +4.3% y/y). As profits are growing, the U.S. economy tends to avoid big trouble. Still, until U.S. economic growth becomes more broad-based (e.g., it includes housing, manufacturing, etc.), it seems critical that government policymakers keep U.S. financial conditions from tightening much. There are some cracks, eg, U.S. home prices declining m/m in June (both the Case-Shiller an… View More