To say the least, since its inception in 1913, the Federal Reserve has had its ups and downs. One thing most people don’t know is that, prior to the invention of the Fed, other than during wars, there was almost no inflation. Various sources , including the Federal Reserve regional banks, show that the purchasing power of $1 in 1900 was the same as or higher than it was in 1800. The Government did print and borrow money during wartime, which caused inflation during the War of 1812 and the Civ… View More

Authors

Fortem Financial

Post 11 to 20 of 629

With roughly 60% of S&P 500 companies having reported, earnings growth estimates have climbed to 27.8%—nearly double the 14.4% expected at the start of the quarter. While mega-cap companies have delivered particularly strong results, growth expectations have improved across every sector except energy. This marks the sixth consecutive quarter of double-digit earnings growth. Equally notable, revenue growth is now exceeding 10%, with broad-based strength across sectors. 2026 full-year earni… View More

The federal government is still on an unsustainable fiscal path, with the national debt reaching $39 trillion in March and poised to rise further in the years ahead as we keep running budget deficits. However, beneath the headlines, both revenue and spending trends have shifted in a positive direction. Its possible investors are recognizing this, which may be helping buoy stock markets. On the tax front, yes, the Big Beautiful Bill enacted last year made permanent many of the temporary tax chan… View More

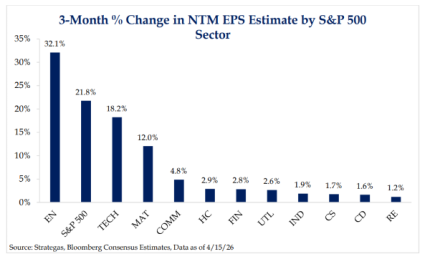

Given sector performance in the first quarter, most people would not be surprised to learn that Energy and Materials were two of the top three contributors to forward upward earnings revisions. What might be surprising is that expectations for NTM earnings in the Tech sector are up by more than 18%, even though the sector's total return was down 9.1% in the first quarter. Multiples for the sector at 23.2x are meaningfully lower than the Industrials and Consumer Discretionary sectors at 25.8x and… View More

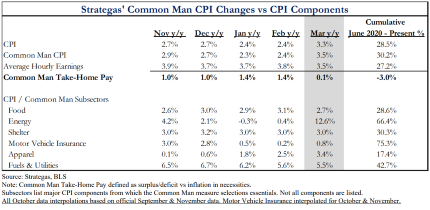

Strategas’ Common Man CPI popped in March amid the energy shock resulting from the U.S war with Iran. As a reminder, the Common Man CPI (CMCPI) consists only of the components people must buy – Food, Energy, Shelter, Insurance, and Children’s clothing. Essentially, it is a “core” measure of inflation in the way a consumer, rather than an economist, would think of it. While the move in our measure m/m was lower than the 0.9% m/m increase of the headline CPI, consumers remain pressured … View More

In 2024, Republicans swept the White House, the Senate, and the House, allowing them to make the Trump tax cuts permanent. But the clock is ticking on their congressional majorities. At this point, we think the odds are very high that the Democrats will win back the House in the midterm election in November. Compared to 2024, the Democrats only need to gain three seats to take back the House. Historically, the party not in control of the White House – this cycle, the Democrats – have gained… View More

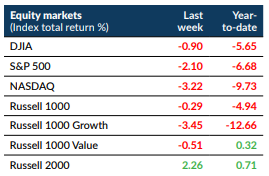

Summary Stocks fell again (S&P 500 -2.10%) (and to the lowest level since September) for the fifth week in a row with NASDAQ down ten of the last eleven weeks. Best sectors were energy (+6.22%), materials (+4.18%), and utilities (+2.94%); worst sectors were communication services (-7.17%) and information technology (-3.44%). Key Takeaways President Trump extended his deadline for a deal with Iran for ten more days. This will likely prolong uncertainty and volatility in the f… View More

Structural forces from electrification to industrial growth are reshaping the U.S. power landscape. We have been commenting on this for the past year or so and have allocated our portfolios accordingly. We thought it may be a good idea to take a little deeper look into Energy considering what is going on in Iran and why this is important to you. After an unusually flat period over the past two decades, U.S. electricity demand is increasing again, marking a meaningful shift from prior consumpti… View More

In the aftermath of the first Internet stock-market bubble of the late 1990s, the economy went into a relatively shallow recession starting in 2001. That recession was precipitated by a tight monetary policy, with the Federal Reserve setting short-term interest rates consistently above the pace of nominal GDP growth (real GDP growth plus inflation). In that sense – as a result of tight money – the 2001 recession was like the recessions of 1970, 1973-74, 1980, 1981-82, and 1990-91. Since tha… View More

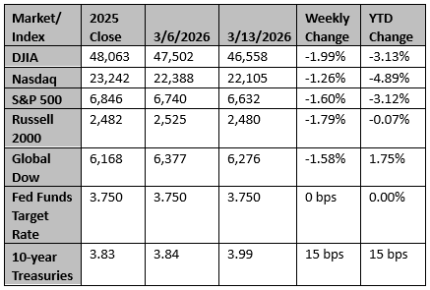

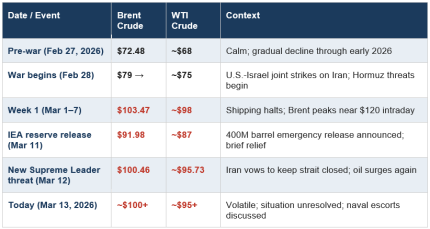

February was a relatively quiet month for markets — the S&P 500 slipped -0.9%, the Nasdaq fell -3.4%, and the Dow edged up +0.2%. Then everything changed on February 28, 2026, when the United States and Israel launched joint military strikes on Iran. Within days, the Strait of Hormuz — the narrow waterway through which approximately one-fifth of the world's daily oil supply normally flows — was effectively closed to shipping. The questions we've been hearing from clients are understan… View More