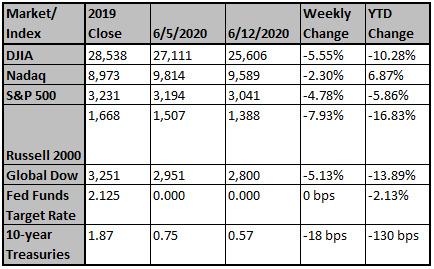

Last week, equities fell for the first time in four weeks. Early last week, cyclicals continued to run from the week before. On Thursday however, risks of a second wave of COVID-19 cases sent the S&P 500 down over 6.8% as investors shed risky cyclical names for relative safety in Information Technology and Communication Services. Friday cyclicals made a slight comeback, but still ended the week negative as Energy, Financials and Industrials were the worst three sectors in the S&P 500. V… View More

Authors

Fortem Financial

Post 371 to 380 of 630

We wanted to share some thoughts on the myriad of news reports floating around and on yesterday's stock market movement. Thursday's stock market movement has many asking, “What made the market drop so much?,” and perhaps more importantly, “Will this look like March all over again?” For the first question, the short answer is that investors appear to have focused on negative (and incomplete) news. For the second question, we believe the answer is NO, and we will provide a basis for that … View More

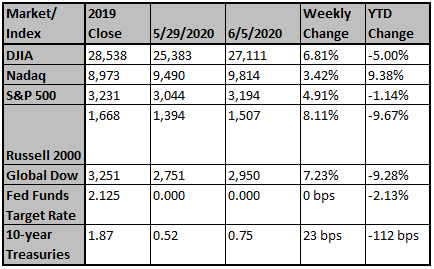

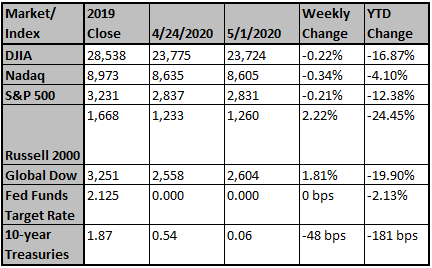

We are indeed living in strange times. After a weekend of peaceful protests and violent riots, stocks opened higher today on optimism for a quicker than expected economic recovery. The S&P 500 closed out last week higher by almost 5%, erasing the losses incurred since the beginning of March. The market recovery was also observed in small and mid-cap stocks where the S&P MidCap 400 and Russell 2000 were both up over 8% last week. Investors eagerly awaited last Friday's job report because … View More

These are indeed interesting times. Our country has been opening back up with great success over the last few weeks, and the economic numbers are starting to reflect a ray of hope for all Americans to get back to NORMAL life. Last week was a decent week for economic data. This statement might seem surprising, given that first quarter U.S. real GDP was revised lower to -5.0% quarter over quarter annualized and tracking estimates for 2Q have fallen to roughly -50% (the Atlanta Fed GDPnow 2Q estim… View More

The S&P 500 Index returned 3.27% last week, gaining back the previous week’s losses. The index is now down less than 7.8% year-to-date and is up over 32.5% since its closing low on March 23. Monday showed its best performance since early April, climbing 3.16% with strength seen in energy stocks as crude oil futures jumped 8.12%. Equity markets were boosted by reports of early positive results from Moderna’s COVID-19 vaccine trial. Positive comments from both Federal Reserve Chairman Jer… View More

With more people spending more time online, cyber security industry experts have observed an increase in cyber security threats. We wanted to share some information on simple things that everyone can do to strengthen their position with respect to cyber security. Please see the attached document to review some recommendations on things you can do to improve your cyber security strength. Sincerely, Fortem Financial(760) 206-8500www.fortemfin.com Latest News Cyber Security Inform… View More

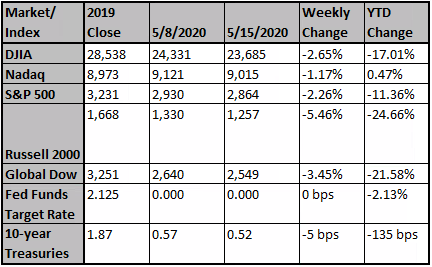

In the middle of last week Federal Reserve Chairman Jerome Powell said the central bank was not considering employing negative interest rates to combat slowing economic conditions. And the data last week did indicate that COVID is wrecking havok with US economic activity. Last Tuesday witnessed a decline in the Consumer Price Index of 0.8% for April. Energy prices declined 10.1% in April, while food prices rose 1.5%. The “core” CPI, which excludes food and energy, declined 0.4% in April, ver… View More

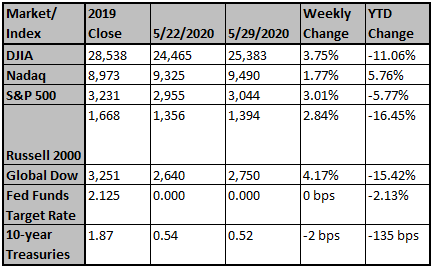

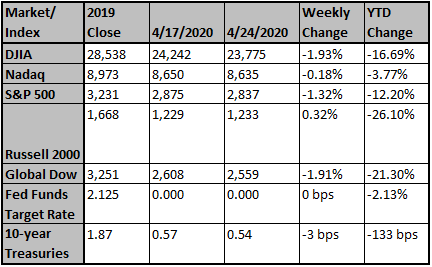

Stocks made a positive move to start off the month with the S&P 500 returning over 3.5% last week, the first positive move since mid-April. Despite stocks moving higher, job losses in April totaled 20.5 million to bring the unemployment rate back to a level not touched since the Great Depression. Investors risk appetites look to be back as technology companies in the NASDAQ Composite index boosted returns to nearly 6% for the week. Fortinet Inc, IPG Photonics, and PayPal Inc were the top tec… View More

Unemployment has surged. There were 152.5 million people on U.S. non-farm payrolls at the peak. The surge in jobless filings during the past 2 months have left U.S. continuing claims at roughly 18 million as of April 18th, up from under 2 million a year ago. Private payroll data (ADP) indicate that roughly half of U.S. workers are employed in small & medium size business – this is where we see continued solvency issues in addition to liquidity issues. Workers can be called back from furlou… View More

US and global leaders have faced difficult decisions over the last month or so. As Covid-19 gained momentum, the US and much of the rest of the world began “sheltering in place,” effectively shutting down significant portions the global economy. There was sound logic in sheltering at home; it would help flatten the contagion curve of the Coronavirus, and with this being a NEW virus, it was the most likely way to flatten the curve within weeks. We needed to protect our healthcare systems and… View More