We wanted to take this opportunity to say thank you for your continued trust in our firm’s Intellectual Capital. Even though we have never been through this type of scenario before, we remain confident that we will get through this and will have a V shaped recovery once we get some clarity on the virus and its effects on the economy in the short-term. We would like to let you know that since the day we founded Fortem, we have built a very robust Technology platform that will allow us to work r… View More

Authors

Fortem Financial

Post 401 to 410 of 630

We continue to hear that the world has NEVER known something like the Coronavirus pandemic, so we decided to do some digging to see what we could find. Interestingly, the first thing we came across was the "H1N1" flu virus. You can access the information yourself from the CDC's website following this link if you would like to: https://www.cdc.gov/flu/pandemic-resources/2009-h1n1-pandemic.html We quote from the CDC, "In the spring of 2009, a novel influenza A (H1N1) virus emerged. It was det… View More

Yesterday was a hard day in the market; some may even contend the market has "never been this bad." But that would be our emotions speaking, and it would be factually incorrect. The S&P 500 was down 9.5%, a far cry from the 22.6% it lost on Black Monday - October 19, 1987. We only bring this up because we believe it provides perspective. It is easy to allow ourselves to believe that the current conditions are the WORST that have ever been. Time (and gains) heal old wounds in the market. The… View More

As many of you know, we have been following Bob Doll for over 20 years now. He put together a list of 10 things to consider during this Coronavirus outbreak. We thought it would worth your time to read his comments, which we have copied below. From his comments, we want to point out the underlying strength in the economy. While we will only know the full extent of what the Coronavirus will do after it is done, we do know that the US economy was about as well prepared for this as one could hope. … View More

We understand the level of fear associated with both the Coronavirus and the market's sudden drop over the last few weeks. Further, we understand the feeling that this is a "new" crisis, the likes of which we've never seen before. In reality, Coronavirus is a new crisis, but that was also true of every crisis we have ever seen. We have been doing this a long time, and we have seen many crises come and go, each of them "new" and "unprecedented." In 1997, we faced the ASIAN FINANCIAL CRISIS. Debt… View More

Over the last few weeks, we’ve heard the comment a number of times that “the world has never seen something like Coronavirus,” and the reference is in relation to more than just the spread of the virus. The reference has been in relation to the market’s movements and to the economic impact the virus will take on the global economy. The genesis of these comments could be a variety of things. We have seen both record daily losses and record gains in the stock market. We have seen the swif… View More

We wanted to share a piece with you that was written by FirstTrust. We think their comments about how various virus's have impacted the markets over the years are worth considering. Please call or email us with any questions. Sincerely, Fortem Financialwww.fortemfin.com(760) 206-8500 Latest News Will We Have a Corona Virus Recession Read Story … View More

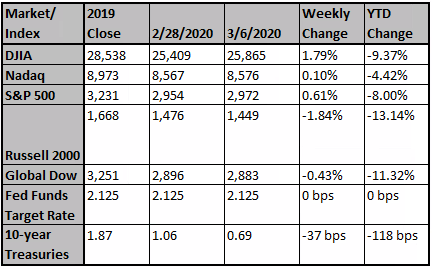

The latest news on the coronavirus and the Super Tuesday primaries caused wild market gyrations last week. Joe Biden’s unexpected primary wins gave him a delegate lead over Bernie Sanders. The coronavirus, however, overtook the Super Tuesday results. China reported a slowing rate of new cases (99 new cases reported on March 6th) for a total of 80,651. Globally, the case count rose to 101,927 with 3,488 deaths. Strategies to contain the virus have led to school closings, work-from-home policies… View More

Last week OPEC and Russia met to discuss cutting oil production by 1.5 million barrels per day; a move in response to slowing demand due to the Coronavirus outbreak in China. Russia decided NOT to participate in the cut, and in response, OPEC has "declared a price war" on Russia and has flooded the market with oil, increasing its production and causing a sharp drop in the price of oil (-30%). Historically, oil has been a proxy for the overall condition of the economy and stock market. This made… View More

The Fed decided to make an inter-meeting move and cut rates -50bp today. The size of the move, as well as the emergency decision, fit with a desire to respond forcibly to evolving market conditions. The FOMC statement read “the coronavirus poses evolving risks to economic activity. In light of these risks and in support of achieving its maximum employment and price stability goals, the Federal Open Market Committee decided today to lower the target range for the federal funds rate by 1/2 perce… View More