At the end of October, we will get our first look at real GDP growth for the third quarter, and it looks like it was solid. We’ll have a more exact estimate a week from now– after this week’s reports on retail sales, industrial production, and home building – but it looks like the economy grew at about a 4.5% annual rate. Even if that turns out right, however, the underlying pace of growth is much slower than what happened in Q3. From the end of 2019 through the third quarter, the avera… View More

Authors

Fortem Financial

Post 151 to 160 of 630

Back in 2008, Ben Bernanke and Hank Paulson, using fear of financial collapse, convinced President Bush and Congress to 1) pass a $700 billion bailout of banks (called TARP) and 2) allow the Federal Reserve to pay banks interest on reserves at the same time the Fed moved from a scarce reserve model of monetary policy to an abundant reserve policy. These policies, to spend and print massive amounts of money, were super-sized during COVID. Both policies proved incredibly damaging. The 2008 financ… View More

Yesterday House Speaker Kevin McCarthy was voted down as House Majority leader by just a few members of his own party and most all members of the opposing party. There are no more Norms in Washington but does the end justify the means. What has been going on in Washington for more than a decade is not sustainable and something needs to change. The last few days in Washington has looked like a circus act. The Government is going to shut down because Congress has not approved spending for next ye… View More

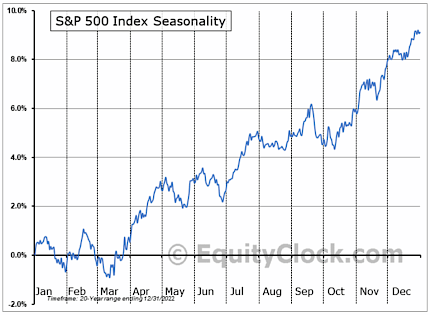

While September had been a bit sloppy, will further weakness in October weigh on investor sentiment before the seasonally strong period begins? As shown by the S&P 500 index seasonality chart below, weakness in the last two weeks of September and the first two weeks of October is common. However, we must also understand that the big down move in the market during that period came from historical crashes such as the “Financial Crisis” in 2008. Excluding those periods, the market still ten… View More

We have plenty of data reports to go, but, so far, the third quarter is shaping up to be a strong one for the US economy. The Atlanta Fed’s GDP Now model is tracking a Real GDP growth rate of 4.9% for Q3, which would be the fastest quarterly growth rate since the earlier part of the COVID recovery. Our models aren’t tracking quite so high but are projecting growth at about a 4.0% rate, still strong by the standards of the past couple of decades. However, we would not get too excited about … View More

The University of Colorado Buffaloes are undefeated and suck up a lot of oxygen in the college football world. After just three games as the new head coach, Deion Sanders was interviewed by 60 Minutes. For now, the Buffs have gone from irrelevant to essential in the college football world. In the competitive arena of sports or business you need to stand out to be noticed. But, when you’re the government, standing out isn’t hard to do. This week, the Federal Reserve is set to release a new s… View More

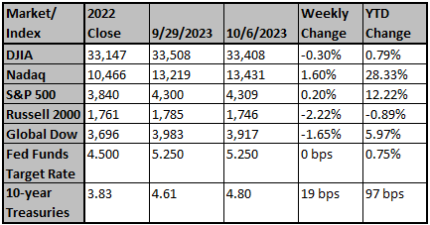

Stocks fell last week (S&P 500 -1.3%) as the S&P 500 and NASDAQ fell below their 50-day moving averages. The market’s mood was primarily defensive with investors focused on the renewed back up in interest rates, dollar strength, and the spike in oil prices. Positive sectors included energy (+1.4%) and utilities (+0.9%); underperformers included industrials (-2.9%) and materials (-2.5%). Source: Bob Doll Crossmark Investments Chart reflects price changes, not total retur… View More

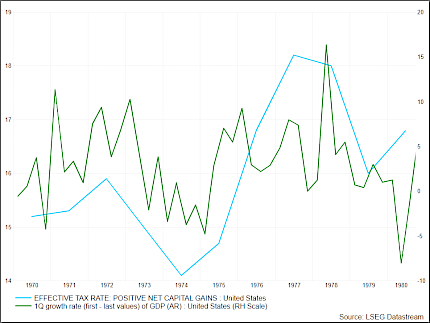

Back in the 1980s, President Reagan took enormous political heat (Sam Donaldson comes to mind) for being fiscally irresponsible. His offense? Presiding over a budget deficit that peaked at 5.9% of GDP in Fiscal Year 1983. But at least Reagan had an excuse. Actually, multiple excuses. The unemployment rate averaged 10.1% in FY 1983, which pushed up spending, while reducing revenue. The Reagan tax cuts were phased-in, so many people pushed off income (and taxes) into future years. Finally, the US… View More

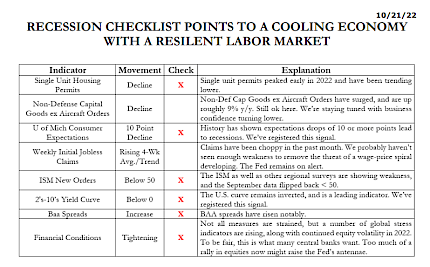

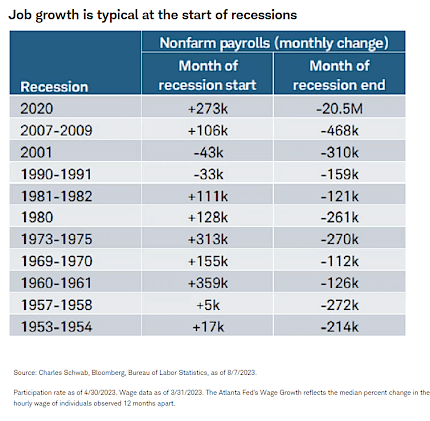

Since the beginning of 2022, the media has regularly warned a recession is coming. As we suggested previously, if a recession did occur, it would be the most well forecasted recession ever on record. Something else has indeed happened. As discussed in numerous measures suggest a recession is forthcoming. However, that recession has yet to reveal itself. Such has led to a fierce debate between the bulls and the bears. The bears contend that a recession is still coming, while the bulls are bettin… View More

Will the economy roll into a formal recession, or is a recovery underway? It's a close call. We've believed all year that the economy has been undergoing a series of "rolling recessions" affecting various industries and sectors. The question is whether it eventually would roll into a formal recession. To date, it's still not clear. Despite the Federal Reserve's efforts to cool economic growth and control inflation, job growth has remained relatively strong—although job expansion historica… View More