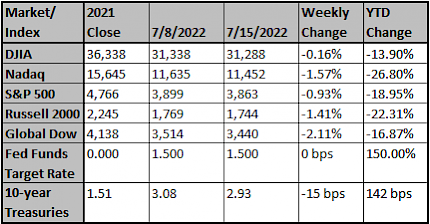

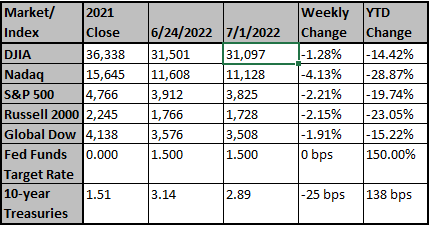

The Treasury yield curve flattened significantly over the course of the week as short-term yields rose and long-term yields dropped while inflation continued to run hotter than expected. The flattening of the yield curve started early in the week as China re-imposed Covid restrictions leading to concerns of additional slowdowns to the world economy. Data released on Wednesday showed the consumer price index increased at a 9.1% year-over-year rate for June, which is the highest annual increase in… View More

Authors

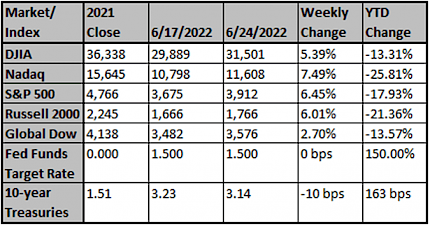

Fortem Financial

Post 231 to 240 of 628

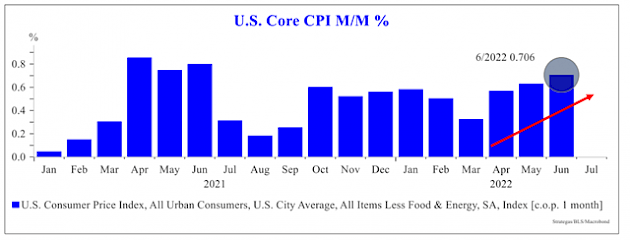

CPI again surged +0.7% m/m (!) and 5.9% y/y. Shelter rose +0.6% m/m. Both core and headline CPI m/m surprised to the upside again this month, indicating inflation has broadened. Bottom line: U.S. inflation is still too high, and monetary policy needs to continue to tighten aggressively in our opinion. Having chosen a +75bp hike last meeting, that should become the default for the July Fed hike at the end of the month. HOW WILL U.S. CONSUMERS DEAL WITH INFLATION? Consider: 1) SMOOTHING THE … View More

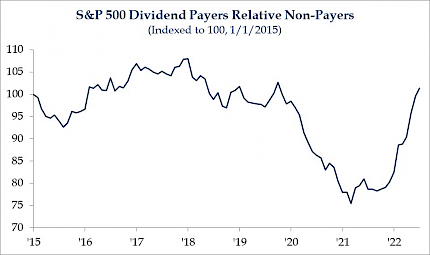

In January 2022 we rebalanced our portfolios to reduce exposure to companies that had extended multiples and were paying little or no dividends. These equities are considered long-duration equities because they will grow into their stock pricing multiples over an extended time period. These companies' stock performance have a history of being very volatile in times of economic slowing and high inflation. In January, we added a number of companies to our portfolio that better met the attributes … View More

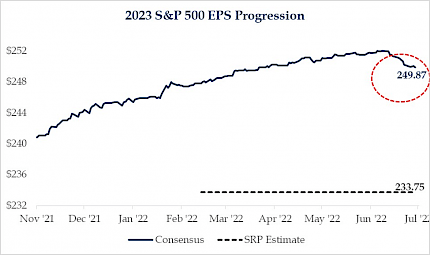

Watching For 2023 Downward Guidance During 2Q Reporting Season The second quarter earnings season is set to begin this week and while earnings are expected to be up about 6%, the 2Q story is about energy holding up the aggregate data. We are more interested in guidance for the remainder of the year and into 2023. We are of the view that 2023 estimates are too high and will likely come in once analysts are given the cover from companies. For 2023, the consensus estimate is near $250, our estimate… View More

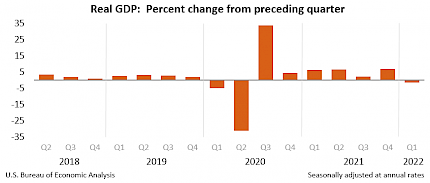

Talk of a Recession is increasing and the yield curve is inverted again. These are usually sure signs that a recession is on the horizon. As with many things these days, the definition of a Recession is ever changing. In the past, the technical definition of a Recession was two quarters or more of Negative Gross Domestic Product (GDP). However, because of the economic disruptions from COVID-19, they have expanded the definition to make it more difficult to say whether we are going into a Recessi… View More

There is continued evidence of a cyclical slowdown. China has already taken a large hit due to local policy decisions. Europe is dealing with the impact of the Russia/Ukraine conflict. The U.S. is feeling the impact of a Fed that has turned aggressive and is aiming for restrictive monetary policy. U.S. initial jobless claims were revised slightly higher & remained above their recent low at 231,000 last week. The U.S. manufacturing PMI new orders component moved into contraction territory at… View More

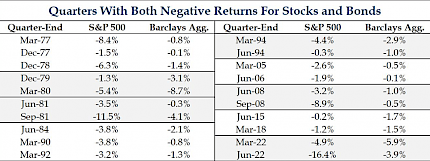

Investors are proceeding into the second half of 2022 with caution after the worst first six months to a year in decades. Risk-off sentiment was seen in most areas of the market, fueled by soaring inflation and the Fed's aggressive monetary policy to fears of slowing growth and increased borrowing costs. A much hoped for "soft landing" also hit some turbulence, with Fed Chair Jay Powell remarking this week "there is no guarantee that we can do that and it's obviously something that's going to be… View More

We've told people to watch the M2 measure of money in order to understand whether inflation will cool down or heat up. The Fed only releases this data on a monthly basis. They used to release it weekly, and we think not doing so robs the world of important information, nonetheless for now it is monthly. Today the Fed released May data on the M2 money supply and from our point of view, it was welcome news, signaling that the monetary surge propelling US inflation numbers to a four-decade high se… View More

Stocks advanced sharply last week (S&P 500 +6.5%), largely reversing the decline of the prior week. The rally stemmed from a technically oversold condition and some evidence that inflation might be peaking. The best performers were consumer discretionary (+8.3%) and healthcare (+8.2%); the worst performers were energy (-1.6%) and materials (+2.7%). WEEKLY ECONOMICS SUMMARY There is developing evidence of a cyclical slowdown. Metals prices (eg, copper) are turning lower. PMI’s are falling… View More

Fear that U.S. has to experience a severe recession to get inflation under control is the ‘wrong lesson’ of history, the St. Louis Fed president says St. Louis Fed President James Bullard spoke in Barcelona. The U.S. economy should continue to grow in the coming several months, said St. Louis Fed President James Bullard on Monday, playing down fear of a severe recession that some economists and market pros view as inevitable in the face of the central bank’s war against too-hot inflation. … View More